By Jen Johnston, CHHC, senior marketing services account manager

It’s been a rocky few months for everyone, and manufacturers of health and wellness products have had their own set of challenges. Here is a quick look at where we’ve been, where we are, and where we might be going.

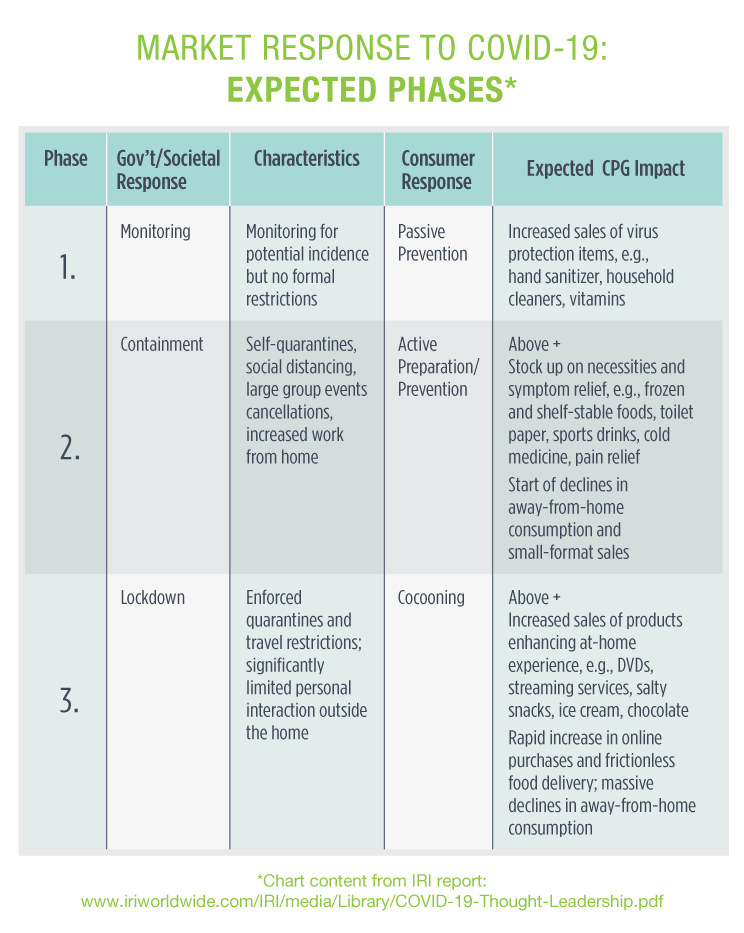

Where we’ve been

In the early days of the pandemic, IRI — a market research company that provides retail insights — released a report called COVID-19: Impact on CPG and Retail. It described the three main phases of market response.

The information proved accurate as communities moved through these three stages. Consumers rushed out to stock up on cleaning products and other sickness prevention items. In short order, they were also proactively snatching up OTC items used for acute symptoms to have on hand “just in case.”

With demand rising so quickly, supply chain challenges for many companies were inevitable. In particular, supplement manufacturers could not produce products fast enough as sales of cold and flu remedies and immune-support products surged. Nutraceuticals World reported that in the first week of March, sales of vitamin C spiked 146%, zinc grew by 255%, and elderberry supplements were up 415%.

Many sources said it was important for brands to keep advertising during this time and we agreed. From a B2C perspective, only 8% of consumers wanted brands to stop advertising. From a B2B perspective, most of our IN.depth Category Spotlight and Product Sampler advertisers stayed present in front of independent pharmacy retailers so that when it comes time for these stores to reorder, their brands are top of mind.

Where we are

In addition to the aforementioned and ongoing supply chain challenges, trade show and buyer meeting cancellations have forced the industry to think and operate differently. Virtual trade shows and buyer meetings via Zoom or Microsoft® Teams are becoming more common place. Our staff at HRG is also adjusting to this virtual work environment. One thing we are already well versed in, however, is how to make a good impression with retail buyers. When you can’t be there in person, your brand’s pitch deck needs to be extremely buttoned up. Learn how HRG can help you update your buyer presentation with category insights, planogram vignettes, and a cohesive and compelling selling story.

Wondering about the current state of online shopping? During the active pandemic, which for many regions included or continues to include lockdowns and curfews, 59% of respondents to a Coresight Research survey acknowledged buying more online than they used to.

Here are a few of the items they reported buying more of online:

- 53% – household products (cleaning items, toilet paper)

- 43% – personal care/hygiene products (soap, handwash)

- 42% – food or non-alcoholic beverages

- 41% – health products (vitamins, medicines)

- 18% – beauty products, cosmetics, fragrance

IRI predicts that as shoppers become more accustomed to online ordering, e-commerce will continue to gain share of wallet. They encourage omnichannel retailers to invest in infrastructure needed to support the demand for additional services.

Due to this current focus on web-based shopping, manufacturers should revisit their brand’s online presence. Have you provided your retail partners with crisp, multi-dimensional, up-to-date product images? Are the item descriptions, features, and benefits consistently presented across all retailer platforms? Do you have compelling, keyword-rich descriptions for Amazon and other sites that grab attention? If not, HRG can help.

As for their in-store shopping trips, consumers tended to shift their grocery trips to weekdays and made fewer visits, but they bought more when they did shop.

Where we might be going

Will post-pandemic consumers shop more online or return to physical stores? Many brands are wondering if they need to shift their long-term retailer strategy. While it is difficult to predict what people will actually do and where they will shop, one survey of 10,000 people by Shopify showed many people are very eager for the return of brick-and-mortar shopping. In fact, 50% plan to visit non-essential retailers within a week of reopening. (Notably, 22% prefer to wait over a month.) In terms of frequency, 58% say they intend to shop as frequently as before the pandemic, while 36% will shop less often.

BOPIS — that bridge between the online and physical store — may be the big winner with nearly 70% of consumers saying that going forward, they will take advantage of buy-online-pickup-in-store options when available. Though 65% say they will make the majority of their non-essential purchases in physical locations rather than via the Internet.

Manufacturers must evaluate their retail executions strategies and determine if they need to shift resources and priorities or continue working go-forward plans that were developed in pre-pandemic times.